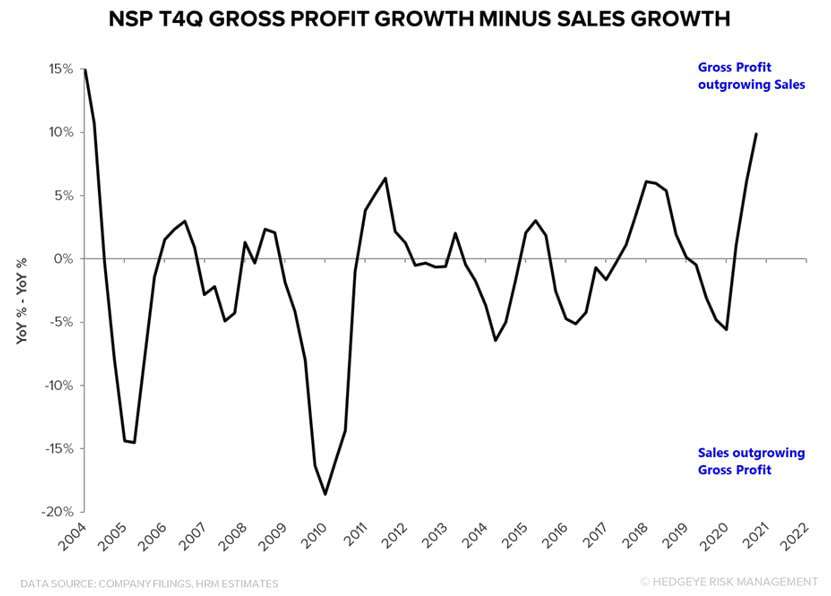

Since we added NSP as a Best Ideas Long and TNET was moved to the long side, NSP shares are up 83% (TNET ~81%) vs the S&P at +39%. While 4Q20 earnings were greatly ahead of estimates and guidance, the shares declined on the loss of a large, low margin customer. That was disappointing and hard to forecast, even if the share price overreacted. We’re most likely near the local high in margin expansion.

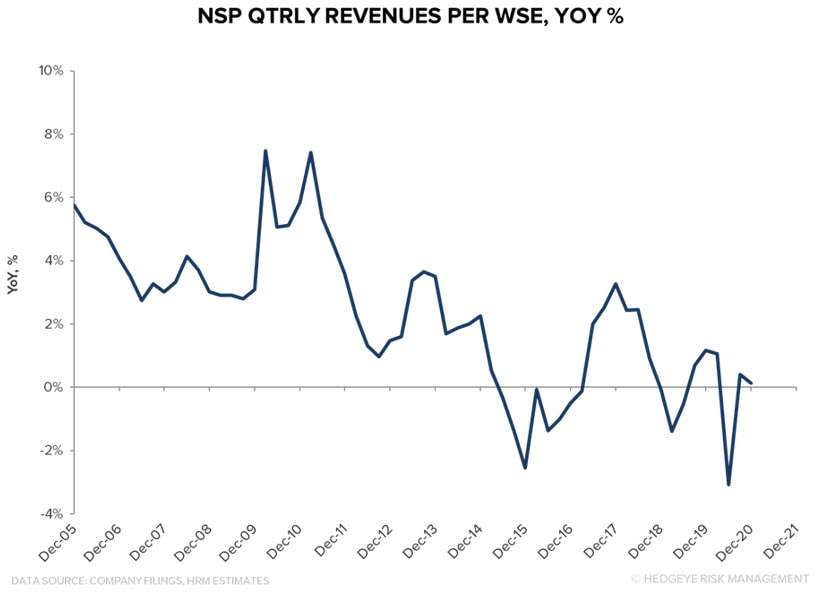

Worksite Employee counts growth held up remarkably well relative to the broader economy, as most of NSP’s workers are in white collar, non-hospitality/travel industries.

NSP/TNET Upshot = Future Short Opportunity Likely: With another 1Q21 beat very likely, we think it is early to add these names back as Best Ideas shorts. We’ll need to see how legislation develops with respect to employment and taxation. But the deferral of medical care that boosted 2020 EPS may well hurt 2H21 results…significantly. Our healthcare team expects higher acuity from patients that avoided medical facilities during the pandemic, with diseases allowed to become more advanced. Mental health spending after the pandemic is also likely to increase. We could well see a situation where NSP and TNET end up ‘cheap’ by end of the year, selling off with soaring benefit costs. A Biden tax plan may bring the next pricing upcycle, but that is a project for a later, better informed decision period.

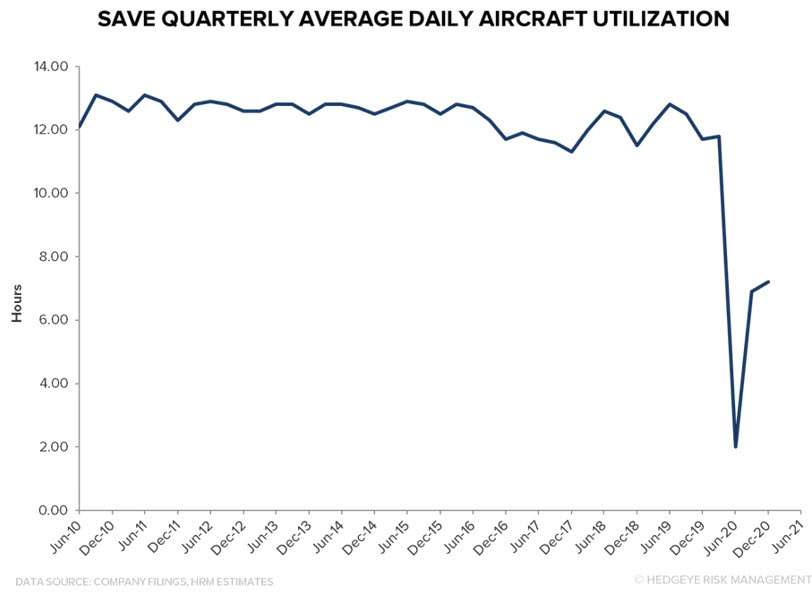

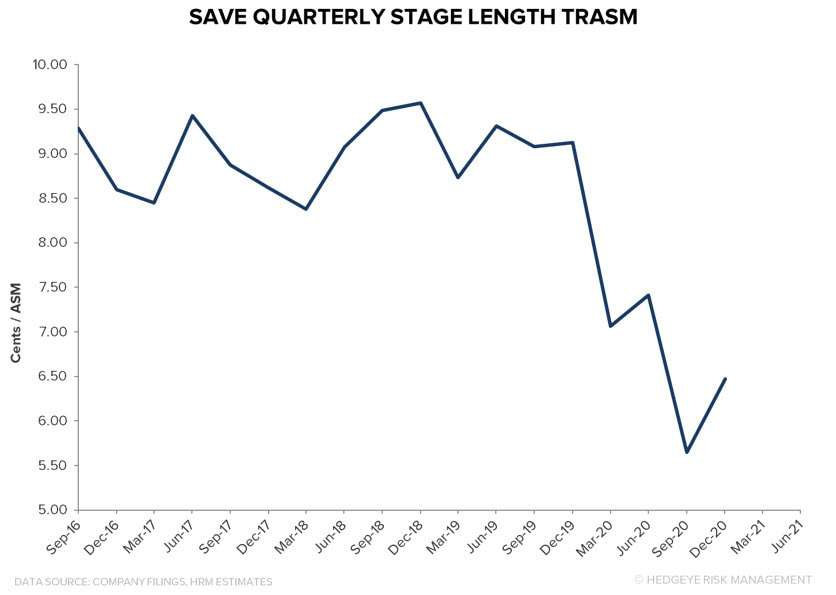

SAVE | Difficult To Imagine Less Relevant Quarter

SAVE shares declined on the print last week, although we aren’t sure anyone should be about 4Q20…or even 1H21…results. It will remain a difficult operating environment until 2H21 and 2022. Aircraft utilization has more room to improve from disappointing 4Q20 levels.

Active app user data continues to improve, perhaps as interested customers fantasy browse…

TRASM ticked higher sequentially by a larger-than-normal amount, with compares easing in 1Q and 2Q 2021.

SAVE shares are up since we added them to Best Ideas, and we expect that outperformance to resume as investors look forward to a pent-up demand, stimulus-fueled leisure travel recovery. We suspect changes in the expected recovery pace are more ‘noise’ than ‘signal’ and see no reason to change our view at present.

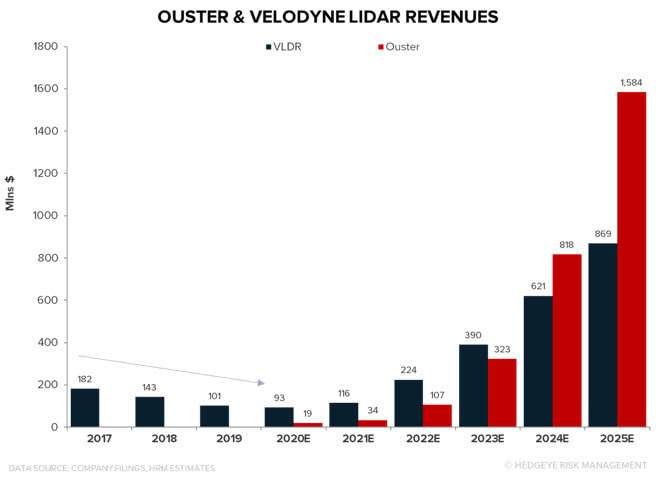

CLA | F Exit Of VLDR Investment Consistent With CLA Thesis

Ford sold its shares in LiDAR maker VLDR…a decision we agree with. GRAF was a SPAC we passed on, with financials that didn’t match the valuation. We doubt that the F exit reflects poorly on LiDAR in general, as Ford is co-invested in Argo AI with VW – the Argo AI system relies on LiDAR. VLDR has a higher cost, ‘legacy’ LiDAR architecture. The company hasn’t grown revenue in years, a financial history that is difficult to reconcile with shareholder enthusiasm for VLDR shares. Instead, CLA expects to take share from VLDR with its cheaper, more scalable custom system-on-a-chip design. While it may initially be viewed as a slight negative for CLA and LiDAR in general, it instead fits with our understanding of the LiDAR state-of-play.

EZ Pass Data | Snow Recovery

EZ pass vehicle counts dropped, as post-holiday weather challenges stalled what was promising improvement.

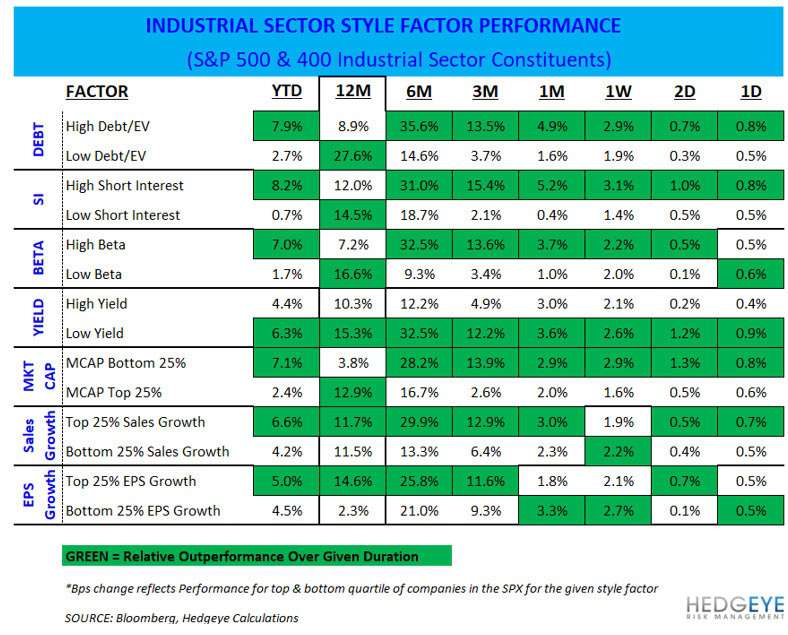

Style Factor Trends Continue To Favor Small Cap, High Beta, High Short Interest Outperformance

Yes, NSP should have been one but specific outcomes aren’t indication of the broader probability backdrop. We’d expect factor exposures to remain in ‘risk on’ territory while we are in Quad 2, anticipating another round of stimulus. On the short side, we continue to favor larger, staples like names (e.g. BLL, SCL) as relative underperformers.